Has Section 87A tax rebate been increased in old, new tax regime in Budget 2024?

No increase has been announced in the tax rebate under Section 87A of the Income-tax Act in the Budget 2024. Tax rebate under Section 87A makes tax payable zero if an individual's taxable income does not exceed the specified level.

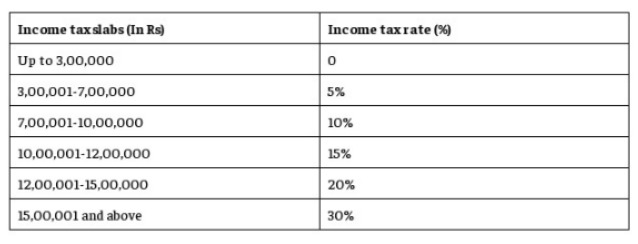

However, the finance minister Nirmala Sitharaman has made changes in the income tax slabs under the new tax regime. As per the proposals, the income tax slabs in the new tax regime will be as follows:

There is a difference in the amount of tax rebate available under the old and new tax regimes. Current income tax laws allow an individual to claim tax rebate of up to Rs 25,000 under the new tax regime and tax rebate of up to Rs 12,500 under the old tax regime.

Due to this tax rebate, an individual having taxable income up to Rs 7 lakh is not required to pay any tax under the new tax regime. Similarly, under the old tax regime, an individual having taxable income up to Rs 5 lakh is not required to pay any tax due to this rebate.

Tax rebate under Section 87A was same under old and new tax regime till March 31, 2023 (FY 2022-23). The higher tax rebate of Rs 25,000 in new tax regime is available from April 1, 2023 onwards.

Who can avail tax rebate under Section 87A

As per the Income-tax Act, the tax benefit under Section 87A is available to individuals who residency status is 'Resident Individuals'. Other categories of taxpayers such as Non-resident individuals (NRIs), Hindu Undivided families (HUFs) and firms are not eligible for tax rebate under Section 87A.

ITR filing mandatory to claim tax rebate

Though the tax rebate reduces tax payable by the taxpayer to zero, it does not mean that filing income tax return (ITR) filing is not required. As per the income tax rules, ITR filing is mandatory if the total income exceeds the basic exemption limit.

There is a difference between the basic exemption limit under the old and the new tax regimes. Currently, the basic exemption limit is Rs 3 lakh in the new tax regime. This is applicable to all individuals (irrespective of their age) who opt for the new tax regime in a financial year.

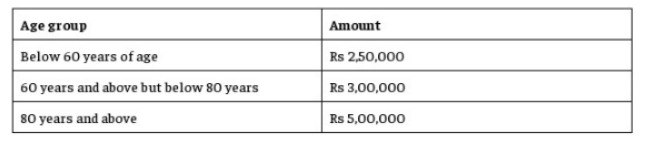

Under the old tax regime, the basic exemption limit depends on the age of an individual in the relevant financial year.

Here is the basic exemption limit for different age brackets under the old tax regime:

How to claim tax rebate under Section 87A

Here is an example to understand how tax rebate under Section 87A of the Income Tax Act can be claimed while filing income tax return.

Suppose a resident individual's taxable income is Rs 7.35 lakh in current FY and the individual decides to opt for new tax regime for FY 2024-25. He is eligible for standard deduction of Rs 50,000 from the taxable income. After claiming standard deduction, the net taxable income is Rs 6.85 lakh. As the net taxable income is below Rs 7 lakh, the taxpayer is not required pay any tax in the new tax regime.

The tax rebate under Section 87A will be claimed as follows:

Step 1: Fill your taxable income under the appropriate head of income in the applicable ITR form.

Step 2: Deduct from this taxable income all deductions and exemptions you are eligible for as per the tax regime chosen.

The ITR form (online or offline utility) will automatically calculate the tax that an individual is required to pay in the online or offline form. The 'Total tax liability' of the ITR form after taking 'Taxes Paid' into account (via TDS, TCS, advance tax or self-assessment tax, if any), will automatically calculate the total tax payable (including cess). The tax rebate (if eligible) will automatically be taken into account in the same section, if the taxable income does not exceed the specified income level of Rs 5 lakh or Rs 7 lakh as the case may be. Hence, the final tax payable amount will appear as zero after tax rebate under Section 87A.